In fact, toys are optional consumer goods, and brands, products, and channels are the competitiveness of toy companies. Although the specific development paths of the toy giants are different, in essence, their success comes from the organic combination of the three.

With the expansion of the domestic toy market and the increasing concentration of the toy industry, domestic leading listed companies will have much to offer, and the three-board enterprises that are still at the end are equally opportunities. Compared with overseas toy companies, domestic listed companies are small in scale and less competitive than overseas leaders. Similarly, compared with the main board enterprises, the competitiveness of the three-board enterprises is generally weak. What is the competitiveness of the three types of enterprises? What are the main differences in their competitiveness? How should the three-board enterprises come to the future?

A domestic toy company started late, and the manufacturing attributes are still significant.

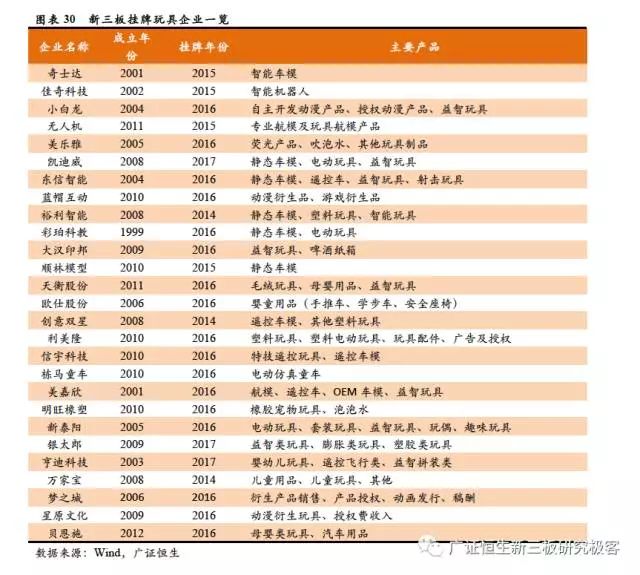

The overseas listed toy segment is represented by overseas listed toy companies with a market share of more than 0.1%, and includes 13 overseas listed companies. The domestic listed toy business sector consists of seven listed companies involved in toy manufacturing. The new three-board toy sector contains 27 listed companies. The specific subject matter is as shown in the table.

Through the comparison between the plates, we found

1. The overseas toy listed company has the earliest establishment time and the longest brand history. The new three board listed toy company was established at the latest, and the brand history is short. The earliest overseas toy listed company was Hornby, a British train model manufacturer. It was founded in 1907 and has been in existence for 110 years. The earliest New Third Board listed company was established in 1998. It has a history of less than 20 years and its brand is relatively young.

2. The overseas toy listed company has obvious consumption attributes. Domestic toy listed companies have stronger manufacturing attributes. Overseas toys produce externally licensed toys or their own IP toys, which are more cultural and consumer. Domestic motherboards and new three-board toy companies are still in the transformation stage. Except for the leading brands such as Aofei Entertainment and Xinghui Entertainment, the products of small and medium-sized toy companies are mainly static models, electronic electric plastic toys, etc., IP and brand. The support is weaker and the manufacturing attributes are more obvious.

As of June 30, 2017, two domestic listed toy companies, Qunxing Toys and Converse Culture, have divested the traditional toy business. However, considering the need to compare the financial data of a toy company for the past three years, the two companies are still included in the analysis.

Comparison of the competitiveness of toy enterprises in and outside the world

The competitiveness of domestic enterprises has increased rapidly!

Revenue scale, profitability and growth rate are the external manifestations of corporate competitiveness. Domestic companies are small but growing rapidly. The three-board enterprise is expected to break out of the main board, and the main board is expected to give birth to the world giant.

1. Domestic toy companies are small but growing fast, and the leading brands of the main board and the three-board high-quality enterprises have become more attractive.

In the past three years, based on the exchange rate of RMB against the US dollar at the end of 2016, the average operating income of overseas listed companies has reached 10 billion yuan, and the average operating income of domestic listed toy companies has reached 1 billion yuan, while the new three board listed companies The average operating income growth was only RMB 100 million. There is a gap of about 10 times between the average revenue scales of the three major sectors. From the perspective of operating income growth rate, the growth rates of NEEQ listed companies, domestic listed companies and overseas listed companies were 34.79%, 6.89% and 5.78% respectively. Although the new three-board companies are currently small, their growth rate is much higher than other sectors.

A similar conclusion can be drawn from the perspective of the net profit of the returning mother. In the past three years, the average net profit of overseas listed companies reached 830 million yuan, much higher than the average size of domestic listed companies of 163 million yuan and three board listed companies of 6.5 million yuan. From the perspective of the net profit growth rate of the returning mother, the domestic New Third Board listed companies have the fastest profit growth rate, and the compound annual growth rate of net profit for the two years is 128.46%. The domestic main board listed companies are second, and the overseas listed companies have the lowest growth rate. It is 5.16%.

From the perspective of growth rate, domestic motherboard companies' revenue and profit scale are expected to move closer to overseas toy companies. Relying on China's huge market scale, domestic toy giants are entirely likely to catch up with overseas leading levels, and the Chinese market is entirely likely to create a world leader. Similarly, the new three board listed companies are also expected to catch up with domestic motherboard companies. The performance of the new three-board head enterprises that broke out from many small and medium-sized enterprises confirmed this judgment. From 2014 to 2016, the operating income of the head-quality enterprises listed on the NEEQ and the net profit of the returning mothers increased faster than the enterprises at the end of the main board. At the same time, the revenue and profit levels of the two types of companies are quite close.

In 2016, the top five companies in terms of operating revenue on the New Third Board have reached the level of half of the companies listed on the Main Board. The top five companies in the net profit of the New Third Board have reached 66% of the companies listed on the Main Board, and they are expected to catch up.

2. The profitability of the giants is strong, and the profitability of high-quality three-board enterprises continues to increase.

From the perspective of gross profit margin, the gross profit margin of NEEQ listed companies ranked the lowest among the three sectors. The gross profit margins in 2014, 2015 and 2016 were 21.90%, 25.34% and 28.74% respectively. The gross profit margin of overseas listed toy companies is the most prominent. The three-year gross profit margin is 45.81%, 45.33% and 44.91% respectively. The gross profit margin of the domestic listed sector is slightly lower than that of overseas listed companies, but in recent years there has been a close trend.

The gross profit margin of domestic and overseas listed toy companies is greatly affected by the pan-entertainment enterprises with large scale and gross profit margin. Since the three boards do not have a pan-entertainment enterprise with outstanding scale and profitability, their gross profit margin is far from the domestic main board listed companies and overseas listed companies.

From the perspective of net interest rate, domestic listed toy companies have outstanding performance. The average net profit rates in the past three years have reached 12.56%, 18.82%, and 17.94%, respectively, which is higher than that of overseas listed companies. Although the net interest rate of the listed companies of the New Third Board is not as good as that of the main board enterprises, it has been greatly improved in the past three years. The average net profit rate in 2016 was 9.17%, which was higher than the average net profit rate of overseas listed companies.

From the perspective of gross profit margin and net profit margin, the overall profitability of the NEE head enterprises is close to the overall level of the companies listed on the main board. It can be seen that the rapid development of the New Third Board enterprises is not based on price wars or sacrificing profits. Despite its small size, NEEQ companies still have strong competitiveness in terms of products and business.

We believe that the main board enterprises are large in scale, have a high market share, and are generally stronger than the new three board enterprises. Although the high-quality target of the New Third Board is not as good as the main board enterprises in terms of revenue, these companies have strong profitability and rapid growth, and they are expected to grow rapidly and compete with the motherboard companies in the future.

Three brand strength comparison -

There is a big gap in brand cultivation operations between domestic and foreign companies!

The three pillars of the consumer industry include brand power, product strength, and channel power. Successful toy giants are always a combination of three forces. Through the comparison of data and case, we will analyze in detail the differences in the competitiveness factors of overseas listed, domestic listed, and new three board listed three toy companies.

1. Self-owned brands have become the consensus of enterprises, and cultivation and operation are the main gaps.

For consumer goods, brand influence is crucial, and toy companies are no exception. A toy company that does not have its own brand cannot have a consumption attribute, and it is difficult to achieve rapid development in the market. According to the statistics of Guangzheng Hang Seng, the toy products of 13 overseas listed toy companies and 7 domestic listed toy companies are all sold under their own brands.

Although the new three-board toy company is not as competitive as the main board of the company at home and abroad, it does not have its own brand among the 25 new three-board listed companies, and only the OEM is the main production mode. Lin model two companies. Most small and medium-sized enterprises have established their own brands. It can be seen that the gap between the new three-board enterprises and the main board enterprises is not whether they have their own brands, but the strength and effect of brand cultivation and operation.

2. Self-owned IP cultivation and operation is an important support for brand building, and the three-board SMEs have a long road ahead.

Own IP is an important fulcrum for brand cultivation and operation. The leading companies headed by Mattel, Hasbro, Lego, and Bandai all pay great attention to the cultivation and operation of the brand. Vertical integration around the core brand, horizontal extension of the brand line is the main growth logic of the toy giant. The cultivation of self-owned IP images is the top priority of these giant brands. Mattel's Barbie, Hasbro's Transformers, Bandai's own IP, etc. have become the brand name of the toy giant. The cultivation and operation of its own IP is an important support for brand building.

Domestic toy leader Aofei Entertainment also pays attention to the creation of its own IP brand. So far, Aofei Entertainment has created 13 cartoon images with independent intellectual property rights. Although these IPs are still difficult to compare with foreign countries, considering that the operation time of Aofei is much shorter than that of overseas leaders, this achievement is not easy. For Gaole shares, Qunxing toys and most of the manufacturing toys companies in the New Third Board, the brand is only an embodiment of intellectual property rights. Without the support of IP or core technology, the construction of brand power is difficult to highlight in a short time. .

The formation of its own IP brand requires long-term cultivation and accumulation. Overseas giants Mattel and Hasbro were established in 1948 and 1926 respectively, and have been 69 years and 91 years old, which is longer than the operation time of most overseas listed companies. The domestic IP giant Aofei Entertainment has also been in operation for 24 years since its establishment, which is far longer than the operation time of most domestic listed companies and listed companies. The cultivation of independent IP, the establishment of the brand is not completed in a short time, and requires long-term operation and accumulation. Domestic manufacturing toy companies are far from the overseas listed companies in terms of the strength and progress of brand building, and it is difficult to achieve overnight.

Four product strength comparison

Domestic enterprise R&D intensity is in a leading position, differentiated products help development

Even in the era of IP being king, product technology is still a core element of toys. In fact, high-quality toy companies never focus on IP operations and ignore product technology. A large number of examples show that a well-designed item will succeed with its innovative properties even without IP. We believe that the company's investment in innovation, research and development, etc. is particularly important in the process of product building. On this basis, relying on its own technological advantages to develop differentiated products is a key step for SMEs to break through.

1. R&D plays a key role in the process of product creation, and the R&D intensity of leading enterprises is higher than that of peers

R&D innovation is the core competitiveness of toy companies. R&D expenditures and R&D expenditures of leading listed companies at home and abroad are ahead of the industry average. The 2016 R&D expenditures of Mattel and Hasbro accounted for the first and fourth place in the overseas toy sector, respectively, reaching 5.31% and 3.55%, which was higher than the industry average R&D expenditure. In terms of the absolute amount of R&D expenditure, Hasbro and Mattel ranked first and second in the overseas toy sector, respectively, at $266 million and $193 million. The growth rate of R&D expenditure in the past three years was 9.40% and 1.10%, respectively, and R&D expenditure continued to increase.

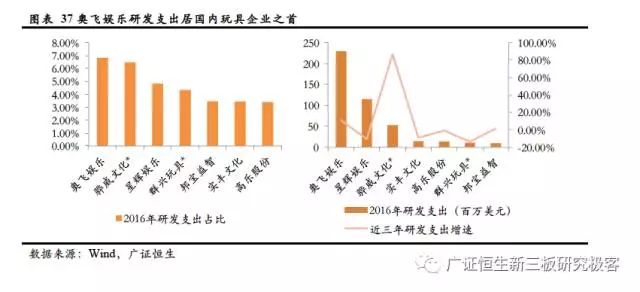

Domestic Aofei Entertainment, Xinghui Entertainment, two pan-entertainment giants starting from the toy industry also showed that the R&D intensity is greater than other toy manufacturing features in the sector. In 2016, the share of research and development expenses of Aofei Entertainment and Xinghui Entertainment was 6.82% and 4.83% respectively. It ranks first and third among domestic toy companies; R&D expenditure is 229 million yuan and 115 million yuan respectively, ranking the top two domestic listed toy companies. Leading Aofei Entertainment's R&D expenditure growth rate in the past three years still reached 11.01%, and R&D expenditure continued to increase. Taking into account the research and development characteristics of leading companies at home and abroad, we believe that R&D investment plays an important role in the process of product building and enhancing the competitiveness of enterprises.

2. The new three-board enterprise has a high proportion of R&D expenditure, and the product will have a strong willingness to build

From 2014 to 2016, the average R&D expenditure of main board companies was 57.28 million, 52.28 million and 63.7 million yuan respectively. Considering that there is a big difference between the business of Aofei Entertainment and Xinghui Entertainment and the new three-board enterprises, the average R&D expenditure of the main board enterprises after the elimination is 13.99 million, 17.9 million, and 20.21 million yuan, and the average R&D expenditure is still significantly higher than the new one. Three board companies. The main reason for this difference is that the size of the new three-board enterprise is smaller than that of the main board enterprise.

The R&D expenditure of the new three-board toy enterprises is generally higher. From 2014 to 2016, the average R&D expenditure of 25 companies in the New Third Board accounted for 5.35%, 5.30%, and 6.33%, respectively, in the three sectors of the New Third Board, the domestic main board, and the overseas market. The middle ranks first and shows a trend of increasing year by year. The average R&D expenditure of the seven domestic listed companies ranked second among the three sectors. The expenditures in the past three years accounted for 4.46%, 4.68%, and 4.69%, respectively, and remained relatively stable. Comparing the difference between R&D expenditures of the new board and the main board enterprises, we believe that although the scale of the new three board enterprises is small, the willingness to build product strength is strong, and the research and development expenditures are relatively high. The research and development intensity is obviously higher than that of the main board enterprises listed at home and abroad.

3. Focus on differentiated market segments to help SMEs break through

Judging from the development experience of overseas toy market, the development path of excellent toy companies is mostly from product to channel, and then from channel to brand. Nowadays, the toy industry is not a highly dispersed state of overseas Hasbro, Mattel and domestic Aofei. The toy industry at home and abroad has gradually shown an obvious head pattern. A considerable number of market segments have been occupied by leading companies.

The top three companies in the net profit of the new three-board toy enterprises are all using the advantages of their own technology and taking the strategy of differentiated competition routes to break through from the tail to the head. The three companies of UAV, Qishida and Jiaqi Technology make use of the technological advantages in intelligent and electronic toy products, focusing on the sub-sectors of three domestic small-scale enterprises involved in aircraft models, intelligent interactive remote-controlled vehicles and intelligent robots. Targeted investment in R&D expenditures above the overall level of the New Third Board, occupying differentiated subdivisions and achieving a leap in corporate performance. In the past three years, the net profit of UAV, Qishida and Jiaqi Technology has reached the second to the first place, the eighth to the third place, and the tenth place in the new three-board enterprises. The second breakout. Operating income exceeded 300 million, and the net profit margin exceeded 30 million. Both indicators ranked within the top six of the new three-board enterprises. It laid the foundation for scale for subsequent development.

Five sales force comparison

The sales force of domestic toy companies is obviously insufficient!

1. Multi-level distribution is still an important part of domestic toy sales, and the use of e-commerce channels is insufficient.

The overseas toy giants mainly use offline retail channels in their domestic markets and distribution in foreign markets. Channels are the battleground for the consumer goods industry. The sales channels of overseas toy companies have similar characteristics: domestic channels are mainly offline retailers, while foreign channels are mainly dealers.

In the United States, for example, Wal-Mart, Toys R Us, and Target's three major retailers are major customers of American toy companies such as Mattel, Hasbro, and JAKKS Pacific. The sales revenues of the three major retailers are in various toys. The total revenue of the manufacturers accounted for more than 40%, and the sales channels were concentrated. In recent years, a major trend in the sales channels of overseas toy companies has been from offline to Internet expansion. By 2016, 17% of toy sales were generated through e-commerce channels. In order to adapt to this trend, Hasbro, Tome, and Bandai have gradually built their own Internet retail channels, improving their responsiveness to the diverse needs of consumers and overcoming the differences in retail environments in different countries.

The brand names of domestic listed and listed toy companies are low. Toy sales channels are mainly multi-level distribution, and there is a big gap between the channel structure of overseas toy companies. The well-known companies such as Aofei Entertainment, Xinghui Entertainment, and Bangbao Puzzle have similar channel structures to overseas toy giants: downstream customers in the local market are mainly retailers, and overseas markets are operated by dealers. For listed companies such as Qunxing Toys and Gaole Co., as well as most of the manufacturing toy companies in the New Third Board, the sales model is still dominated by traditional multi-level distribution, and the first-tier dealers are its main downstream customers. Domestic e-commerce channels are developed, and more than 20% of toy sales are generated through e-commerce channels. However, the use of e-commerce channels by the new three-board toy manufacturers is still insufficient. Only five of the 24 companies have clearly indicated that they have established self-operated e-commerce channels in China.

2. The marketing efforts of domestic enterprises are obviously insufficient, and the sales force is gradually becoming elbow

From 2014 to 2016, the average sales expenses of listed companies in the New Third Board accounted for 4.05%, 4.42%, and 5.59%, respectively. Ranked last in the three categories of companies. In the same period, the average sales expenses of domestic listed toy companies accounted for 6.97%, 8.42%, and 8.44%. The two companies of Aofei Entertainment and Xinghui Entertainment played an important role in the sales cost ratio. The proportion of advertising expenses of listed companies in foreign countries is similar to the proportion of sales expenses of domestic listed companies, but advertising expenses are only part of the sales expenses. Therefore, overseas listed companies have higher investment in marketing. This shows that the marketing efforts of the new three-board toy companies are obviously insufficient.

The emergence of this phenomenon is closely related to the channels of toy companies. Domestic toy companies mostly use multi-level distribution as the main business model. The company has established strong business cooperation with a small number of first-tier dealers, and the expenditure on the sales link is relatively low, so the sales expenses of the three-board enterprises account for a relatively small proportion. The multi-level distribution model makes the value loss of toy products in the circulation link larger than that of direct sales and retail channels, which is related to the late start of the domestic toy industry, weak brand in the early stage of development, and insufficient product competitiveness. With the enhancement of the brand awareness of domestic toy companies and the increasing investment in product research and development, the lack of sales power has gradually emerged. We believe that sales force is the key to domestic toy companies to improve their competitiveness in the short term.

Six brands, sales gap is obvious

After the differentiation breakout, strengthening sales force is a short-term goal!

1. The strength of research and development is in a leading position, and the brand and sales gap are obvious.

Brand strength, product strength and sales force are the core sources of toy enterprise competitiveness. Domestic and foreign companies have a large gap in brand power and sales power, and the gap in product power is not obvious.

In terms of brand power, there is a big gap between domestic and foreign companies. The formation of a brand takes time to accumulate and also requires IP support. Because China's toy industry started late and the company is relatively young, it can't compare with overseas leading enterprises in terms of business time, and it has not enough resources and ability to create a hot IP that can support the brand. Therefore, the new three-board enterprises and domestic listed companies There is still a big gap between brand power and overseas listed companies.

In terms of product strength, the gap between domestic and foreign companies is not obvious. From the perspective of R&D expenditure, overseas listed companies and domestic listed companies have obvious advantages due to their large scale. However, from the perspective of the proportion of R&D expenditure, the R&D expenditure of the NEE toy companies accounted for the largest proportion, and it still showed a trend of continuous strengthening. It can be seen that domestic small and medium-sized toy enterprises pay more attention to R&D investment, and the efforts to build product strength are more and more strengthened. In the foreseeable future, China's toy companies will be expected to compete with foreign leaders in product technology.

In terms of sales force, domestic toy companies and overseas toy companies also have a certain gap. The main customers of overseas toy companies are large retailers. The products are delivered directly to the retail chain after delivery, with low value loss and fast circulation. At the same time, large-scale retail sales are beneficial to the brand of the enterprise. The main customers of domestic toy companies, especially the new three-board toy companies, are mainly first-class dealers, which realize the circulation of goods in a multi-level distribution mode. This model is costly in the circulation process, and the circulation speed is slow. The uncertainty of the terminal seller is not good for brand building.

2. The development path of SMEs: differentiated breakout, early focus on sales promotion, medium and long-term focus on brand building

Taking Hasbro as the benchmark, the long-term focus of domestic leading companies such as Aofei is to use the capital market to deep integration around IP. Focus on the organic integration of IP and various pan-entertainment businesses, focusing on “chemical reactions†rather than simple “physical combinations†and further developing towards the world giants. For the development strategy of domestic giants, this article will not be analyzed in detail, and the focus will mainly be on the road to break through the SMEs of the New Third Board.

The development path of SMEs will be based on product differentiation and break through to the level of 2-3 billion revenues. Early attention will be paid to the improvement of sales channels, and the medium and long-term focus on brand building. SMEs listed on the three boards attach great importance to product research and development, and the R&D intensity is even ahead of overseas leaders. Although the difference in scale makes the absolute value of R&D expenditure of domestic enterprises less than that of overseas toy companies, it is excellent in terms of R&D intensity. In the process of product creation, SMEs need to focus on the breakthrough of the differentiated competition route. Targeting the niche market under the head pattern, the company launched a burst of funds through technology differentiation and IP differentiation to achieve a breakout of RMB 200-300 million from the tail to the revenue. For example, VR/AR + remote control car and the current popular king glory + toy, wolf + toy and other concepts may form explosive models, helping toy companies to expand rapidly.

Toy companies at home and abroad have a big gap between brand power and their own IP operations, but they are not without advantages. Compared with foreign countries, China's long history and culture as well as the contemporary developed Internet industry provide rich materials for the self-owned IP of China's toy companies. The integration with domestic high-quality content will likely create a burst of funds and help enterprises complete the tail. Break ahead and enhance the brand effect. It is true that the creation of brand power is not a one-off event. Enterprises need to have long-term accumulation and sufficient scale and resources to complete the cultivation or acquisition of IP. In order to build a core brand, overseas giants have spent decades. We believe that for brand building, small and medium-sized toy companies do not have the conditions to improve in the short term, and more importantly, they will combine the advantages of IP materials for brand accumulation and construction. Leading companies are expected to combine the domestic history and culture with the advantages of Internet content, actively use the capital market to do deep M&A integration, enhance IP operation capabilities, launch explosions and form or consolidate head advantage.

Relative to brand power and product strength, domestic toy companies should pay attention to the creation of sales force in the short term. With the overseas leader as the reference system, the rise of Hasbro and Mattel in the 1950s is inseparable from its product marketing investment. Both giants are actively using new marketing methods to improve product sales. In 1955, Hasbro's classic product, Mr. Potato Head, became the world's first product to be marketed through TV commercials.

In the same year, Mattel signed a one-year advertising agreement with the Disney Channel to promote its products in the “Mickey Mouse Club†program. We believe that it is reasonable to improve the sales link as the short-term goal of China's toy companies. How do you do that?

1. Actively deploy domestic channels

With its own brand, it embraces the toy market where domestic large space is concentrated.

2. Leverage the Internet

In the construction of channels, taking into account the differences in channels between domestic and foreign toy companies and the mature online retail system in China, domestic toy companies should gradually reduce their dependence on distribution channels, and leverage the domestic mature and advanced Internet retail model to promote the line. Direct sales channel construction.

3. Enhance the importance of marketing efforts

Leveraging the mature mobile marketing model of the Internet, we will increase marketing efforts in various aspects, and drive the rapid expansion of scale with the increase of sales force to realize the process from quantitative change to qualitative change.

Source: Guangzheng Hengsheng New Third Board Research Geek

Sewing thread is the thread required for knitted clothing products. According to the raw materials, sewing thread can be divided into natural fiber, synthetic fiber and mixed sewing thread. With the development of polyester industry, more and more pure polyester fibers are used as raw materials for sewing thread.

Sewing thread refers to the thread used for sewing textile materials, plastics, leather products, books and periodicals, etc. The sewing thread has the characteristics of seamability, durability and appearance quality. Sewing thread is generally divided into three types: natural fiber type, chemical fiber type and mixed type due to different materials; The characteristics of sewing thread also have its unique performance due to different materials:

Cotton sewing thread

---Good heat resistance, poor elasticity, abrasion resistance, moisture resistance and bacteria resistance, suitable for high-speed sewing and durable pressing.

Long staple pure cotton thread is mostly used: it is made of long staple cotton through combing, singeing and mercerization, and it is twisted with high density, so the tension is better than ordinary combed pure cotton. It is often used for sewing pure cotton clothing and other pure cotton fabrics.

Pure cotton thread: It is generally divided into two parts: ordinary combed and combed. The real 100% pure cotton thread can be used for sewing is fully combed cotton. Generally, 402, 202 and 203 are used. It is made of combed and singed high-quality cotton in cotton area. Pure cotton thread is often used for sewing pure cotton clothing and other pure cotton fabrics.

Sewing Threads and Yarns,Cotton Sewing Thread,Polyester Sewing Thread,Sewing Machine Thread,Embroidery Thread

OYEAL Global , https://www.oyeal-home.com